You check your credit report and see an unfamiliar entry: “CCS Collections” or “Credit Collection Services.” Your score has dropped, possibly by 60 to 100 points, and you’re not sure what to do next. You’re not alone, and more importantly, this situation is not hopeless.

CCS collections on your credit report can feel overwhelming, especially if aggressive agents are calling you. But knowing exactly what CCS is, understanding your consumer rights, and following the right removal strategy can make a significant difference. At The Phenix Group, our attorney-powered credit repair specialists help clients navigate situations exactly like this every day.

This guide covers everything you need to know: what CCS is, why it appears on your report, how badly it hurts your score, and most importantly, the proven steps to remove it.

What Is Credit Collection Services (CCS)?

Credit Collection Services, commonly known as CCS, is one of the largest third-party debt collection agencies in the United States. Headquartered in Norwood, Massachusetts, CCS employs over 700 people and collects debts across multiple industries including:

- Banking and financial services

- Healthcare and medical billing

- Insurance

- Utilities

- Government and municipal services

You may see CCS appear on your credit report under several different names: CCS Offices, CCS Collection, CCS Payment, CCS Commercial, CCS Companies, or CCS Credit Collection Services. They are all the same entity.

CCS operates in one of two ways: they are either hired by your original creditor to collect the debt on their behalf, or they purchase your debt directly from the creditor for less than the full amount owed. Either way, once CCS is involved, you now owe them, and they have the legal right to attempt collection and report to the credit bureaus.

Why Is CCS Appearing on My Credit Report?

CCS appears on your credit report when an original creditor, such as a hospital, utility company, or bank, gives up trying to collect a past-due account themselves and either sells it to CCS or hands it over for collection. This typically happens after an account becomes seriously delinquent, often 90 to 180 days past due.

Once CCS reports the collection account to Equifax, Experian, or TransUnion, it creates a new negative item on your credit file. Even if you had no idea this account existed, it can begin damaging your score immediately.

Not sure which collection agency holds your debt? Our related guide on how to find out which collection agency you owe can help you trace the account back to the original creditor.

How Much Does CCS Hurt Your Credit Score?

A collection account from CCS can cause a significant drop in your credit score, often between 60 and 100 points, depending on your overall credit history. The impact is largest if your score was previously good (700+), because you have more to lose.

Here is why collection accounts are so damaging:

- Payment history accounts for 35% of your FICO score, the single largest factor

- A collection signals to lenders that you failed to repay a debt, which makes you a higher-risk borrower

- The account can stay on your credit report for up to 7 years from the date of first delinquency

- Even paying it off does not automatically remove the entry, it only changes status to “paid collection,” which still harms your score

This is why simply paying CCS without negotiating removal is rarely the best strategy. You want the account gone, not just marked paid. For related context, our article on how long before a collection agency reports to the credit bureau explains the timeline in detail.

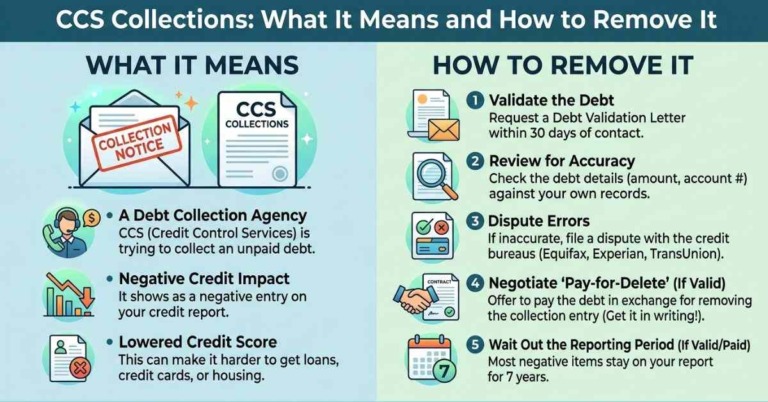

How to Remove CCS Collections from Your Credit Report

There is no single magic fix, but there are four proven strategies for removing CCS from your credit report. The right one depends on whether the debt is valid, how old it is, and whether you have already paid.

Step 1: Pull Your Credit Reports from All Three Bureaus

Before doing anything, get your free credit reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com. Check all three, CCS may be reporting to one bureau and not another, or reporting different amounts. Document any inconsistencies, wrong dates, incorrect balances, or accounts that do not belong to you. These are potential dispute grounds.

Step 2: Send a Debt Validation Letter Within 30 Days

Under the Fair Debt Collection Practices Act (FDCPA), you have the right to request that CCS prove the debt is valid and belongs to you. This is called debt validation. You must send this request in writing, via certified mail, within 30 days of first being contacted by CCS.

In your letter, request the following: the name of the original creditor, the exact amount owed including fees, the date the account became delinquent, and proof that CCS has the legal right to collect this debt. If CCS cannot validate the debt, they are required by law to stop collection efforts and remove the negative entry from your credit report.

Remember: CCS often purchases debts in bulk, and original documentation is frequently incomplete or inaccurate. Do not assume the debt is valid just because CCS says it is.

Step 3: Dispute Errors with the Credit Bureaus

If your credit report contains inaccurate information about the CCS account, wrong amount, wrong date, wrong status, you have the right under the Fair Credit Reporting Act (FCRA) to dispute it directly with the credit bureaus. Each bureau (Equifax, Experian, TransUnion) is required to investigate and correct or remove the disputed information within 30 days.

Our article on whether disputed collections can come back on your credit report explains what to do if a removed item reappears.

Step 4: Negotiate a Pay-for-Delete Agreement

If the debt is valid and within the statute of limitations, a pay-for-delete agreement is one of the most effective removal strategies. This is where you agree to pay CCS, often less than the full balance, in exchange for their agreement to delete the collection entry from your credit report entirely.

Important tips for negotiating pay-for-delete with CCS:

- Start by offering 40-50% of the balance, CCS typically purchased the debt for far less

- Never agree verbally, get the full terms in writing before making any payment

- Do not give CCS direct access to your bank account

- After payment, check your credit report 30-45 days later to confirm deletion

Note: CCS does not always agree to pay-for-delete. If they refuse, a professional credit repair service can often negotiate more effectively on your behalf.

Step 5: Request a Goodwill Deletion (If Already Paid)

If you already paid the CCS debt but the collection entry remains on your report, you may be able to request a goodwill deletion. This is a letter explaining your circumstances, acknowledging the debt, and respectfully asking CCS to remove the entry as an act of goodwill, especially if your payment history since then has been positive.

Goodwill deletions are not guaranteed, but they do work in some cases, particularly for one-time mistakes on otherwise clean credit histories.

Your Rights Under the FDCPA When Dealing with CCS

The Fair Debt Collection Practices Act gives you powerful protections against aggressive or illegal collection tactics. CCS, like all debt collectors, must follow strict rules:

- They can only contact you between 8:00 AM and 9:00 PM your local time

- They cannot use threatening, abusive, or obscene language

- They cannot falsely claim to be attorneys, law enforcement, or government officials

- They cannot threaten arrest or imprisonment for an unpaid debt, this is illegal

- They must send a written Notice of Debt including complete details and your rights

- They must stop collection efforts if they cannot validate your debt

- They cannot contact your employer except to verify employment or garnish wages after a court judgment

If a CCS representative has violated any of these rules, you can file a complaint with the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC). You may also have grounds to file a lawsuit against them. Our team has experience dealing with FDCPA violations and can guide you through this process. For a related example of consumer rights in action, see our guide on Professional Credit Services and your rights.

What Happens If You Ignore CCS Collections?

Ignoring CCS is one of the worst decisions you can make. The collection account can continue reporting to credit bureaus, damaging your score for up to seven years, while CCS may escalate to more aggressive collection efforts. In some cases, they can even file a lawsuit against you, even for relatively small amounts.

If CCS wins a judgment in court, they may be able to garnish your wages or place a lien on your assets. A court judgment also becomes a separate negative entry that can further harm your credit score. The debt does not disappear by ignoring it, so addressing it early, even if you cannot pay in full, gives you far more options than waiting.

Statute of Limitations: Does It Apply to Your CCS Debt?

The statute of limitations determines how long a creditor or collector can legally sue you to collect a debt. This varies by state, typically ranging from 3 to 6 years. Once the statute of limitations expires, CCS cannot win a lawsuit against you.

Important nuances to know:

- The clock starts from the date of your last activity on the account, not when CCS bought the debt

- Making a payment or even verbally acknowledging the debt may restart the clock in some states

- The expiration of the statute of limitations does NOT remove the item from your credit report, the 7-year rule is separate

- Do not make any payment to CCS on an old debt without first consulting a professional, as it could restart the statute of limitations

Frequently Asked Questions

Does CCS do pay for delete?

CCS does not widely advertise a pay-for-delete policy, but it is possible to negotiate one. Success depends on the age and amount of the debt, and whether CCS’s collector agrees. Working with a professional credit repair service significantly improves your chances because they know the negotiation process and have established protocols.

Is Credit Collection Services a legitimate company?

Yes, CCS is a legitimate, licensed debt collection agency that has been in business for over 50 years. However, having over 2,000 CFPB complaints and more than 1,000 BBB complaints, many for FDCPA violations, means you should always know your rights when dealing with them.

Will paying CCS remove it from my credit report?

Not automatically. Paying CCS typically changes the account status from an unpaid collection to a paid collection, which still harms your credit score. The only way to have the entry removed is through a pay-for-delete agreement, a successful dispute, or a goodwill deletion request.

How long does CCS stay on my credit report?

A CCS collection account can remain on your credit report for up to 7 years from the date of first delinquency with the original creditor, regardless of whether it has been paid.

Can CCS sue me?

Yes, CCS can sue you as long as the statute of limitations in your state has not expired. If they win a judgment, they can potentially garnish wages or place liens on assets. This is why addressing the debt proactively is critical.

What is the CCS phone number?

CCS can be reached at 617-965-2000 or through their website at ccsusa.com. However, before calling CCS directly, we strongly recommend validating the debt and understanding your rights. A credit repair professional can communicate with CCS on your behalf.

Can I remove CCS without paying?

Possibly. If CCS cannot validate the debt, if the information on your report is inaccurate, or if the statute of limitations has expired, you may be able to remove the account without paying. Working with an attorney-powered credit repair service gives you the best chance of achieving this outcome legally.

How The Phenix Group Can Help You Resolve CCS Collections

Dealing with CCS collections on your own is stressful and time-consuming. Our attorney-powered credit repair team at The Phenix Group takes a different approach than most credit repair companies. We do not just file generic disputes, we engage directly with original creditors, collection agencies like CCS, and all three credit bureaus simultaneously.

Here is what sets us apart:

- Attorney-backed process: We use legal tools and consumer protection laws to challenge inaccurate or unverifiable CCS reporting

- Aggressive multi-front approach: We contact CCS, the credit bureaus, and original creditors at the same time

- Custom strategy: Every credit profile is different, we create a personalized plan based on your specific CCS debt situation

- Experienced team: Our analysts are well-versed in FDCPA, FCRA, and debt negotiation

Whether your goal is to remove CCS to buy a home, qualify for a car loan, or simply improve your financial standing, our credit repair services are designed to deliver permanent, real results.