Before you sign with any credit repair company, including The Phenix Group, you should know the federal law that governs this entire industry. The Credit Repair Organization Act (CROA) is your legal shield against scams, false promises, and predatory practices in the credit repair space. Understanding it makes you a smarter, safer consumer.

What Is the Credit Repair Organization Act?

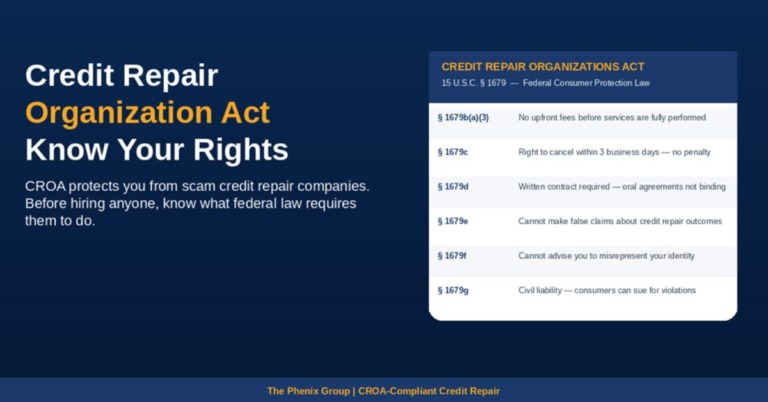

CROA (15 U.S.C. § 1679 et seq.) is a federal law enacted in 1996 as part of the Consumer Credit Protection Act. It was created specifically to regulate companies that offer credit repair services and to protect consumers from fraudulent or misleading claims. CROA applies to any organization that provides, or offers to provide, services to improve a consumer’s credit record, history, or rating, for payment.

Before choosing among different credit repair packages, it’s important to understand the legal protections CROA provides.

: Everything You Need to Know 1")

What Does CROA Prohibit Credit Repair Companies From Doing?

Under CROA, a credit repair organization is explicitly prohibited from:

- Making any false or misleading statement to a consumer or to any person who has extended credit to a consumer

- Advising any consumer to make any statement that is untrue or misleading to a credit reporting agency

- Advising any consumer to alter their identity to conceal adverse credit history

- Charging or receiving any money before fully performing all promised services

- Claiming it can remove accurate and verifiable negative information from a credit report, though legitimate firms may help consumers remove derogatory items that are inaccurate or outdated

What Are Your Rights as a Consumer Under CROA?

- Right to a written contract before any services begin

- Right to a 3-day cancellation window (cooling-off period) with no penalty

- Right to receive a detailed disclosure statement explaining your rights

- Right to dispute any information in your credit file directly with the bureaus yourself, for free

- Right to sue a CROA-violating company for actual and punitive damages

Consumers exploring local solutions like credit repair Odessa TX services should make sure those providers follow every CROA requirement.

Red Flags, Signs a Credit Repair Company Is Violating CROA

- They demand upfront payment before doing any work

- They ‘guarantee’ specific score increases or promise to remove accurate negative items

- They suggest you dispute everything on your credit report regardless of accuracy

- They advise you to use a different Social Security number or create a ‘new credit identity’ (this is federal fraud)

- They don’t provide you with a written contract or disclosure of your rights

- They have no physical address, no licensed professionals, and no verifiable track record

: Everything You Need to Know 2")

How The Phenix Group Complies With Every CROA Requirement

At The Phenix Group, CROA compliance isn’t a checkbox, it’s the foundation of how we operate. Here’s our commitment:

- We provide full disclosure of your consumer rights before any engagement begins

- We provide a clear, written service contract that specifies exactly what we will do

- We honor the 3-day cancellation right without question

- We NEVER charge upfront before services are rendered

- We NEVER promise to remove accurate, verifiable information, our work is legal and ethical

- Our process is backed by attorney-engaged legal oversight, ensuring FCRA and FDCPA compliance at every step

Frequently Asked Questions

Q: Does CROA apply to nonprofit credit counseling agencies?:

A: CROA specifically exempts nonprofit organizations, 501(c)(3) status in particular. However, if a company claims to be nonprofit but charges substantial fees, verify their actual tax-exempt status before proceeding.

Q: What if a credit repair company violated my CROA rights?:

A: You may be entitled to recover any money paid to the company, additional damages, and attorney’s fees. File a complaint with the Consumer Financial Protection Bureau (CFPB) and consult a consumer protection attorney.

Q: Is it better to repair my credit myself rather than hire a company?:

A: DIY credit repair is absolutely an option, and CROA exists partly to remind you of that right. However, professional firms like The Phenix Group bring legal expertise, established relationships, and the capacity to handle complex multi-bureau disputes more efficiently. See our analysis of whether credit repair services really work for an honest assessment.