A collection account on your credit report can feel like an anchor dragging down your financial future. It lowers your credit score, sometimes by 50 to 150 points, making it harder to get approved for mortgages, auto loans, or even a new apartment. The worst part? Collections can legally stay on your report for up to seven years from the date of first delinquency.

But here’s what most people don’t know: you don’t have to wait. There are legitimate, legal strategies that can remove collections from your credit report much sooner, if you know your rights and follow the right process.

In this guide, the credit specialists at The Phenix Group walk you through every proven method for removing collection accounts, whether the debt is inaccurate, outdated, or even valid.

What Is a Collection Account and How Does It Hurt Your Credit?

When you fail to pay a debt, a credit card bill, medical expense, or personal loan, the original creditor typically waits 90 to 180 days before taking action. At that point, they either assign the debt to a third-party collection agency or sell it outright, often for pennies on the dollar. The collection agency then reports the account to Equifax, Experian, and TransUnion.

That single action creates a “collection account” on your credit report, and the impact on your score is immediate and severe. Even one collection can push a good credit score into “poor” territory overnight.

| Starting Score | Estimated Drop | Score After Collection |

| 750–800 (Excellent) | 100–150 points | 600–700 |

| 680–749 (Good) | 75–100 points | 580–674 |

| 620–679 (Fair) | 50–75 points | 545–629 |

| Below 620 (Poor) | 25–50 points | Below 595 |

Even after you pay a collection, it doesn’t disappear. It simply updates to “paid collection.” Newer scoring models (FICO 9, VantageScore 4.0) treat paid collections more favorably, but most mortgage lenders still use FICO 8 — where a paid collection still damages your score. That’s why understanding how long after paying off collections your credit improves is so important before you make any payment decisions.

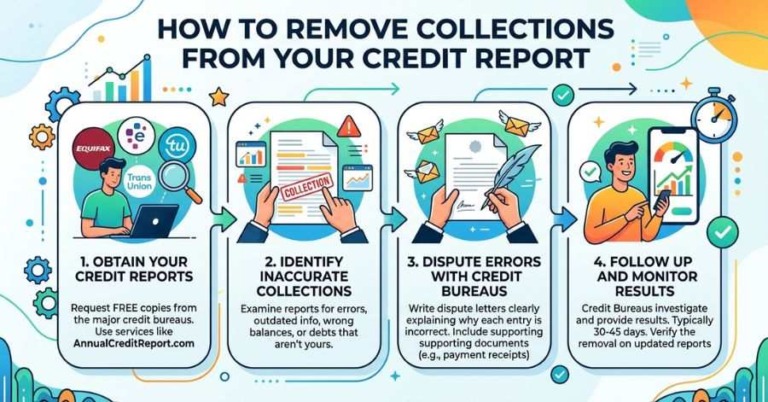

Step 1: Pull Your Credit Reports From All Three Bureaus

Before taking any action, you need to know exactly what you’re dealing with. Each bureau, Equifax, Experian, and TransUnion, maintains its own version of your credit file. A collection may appear on one, two, or all three reports, sometimes with different balances, dates, or statuses on each.

Where to get your free reports:

- AnnualCreditReport.com – the only federally authorized free credit report site (weekly access available through 2026)

- Equifax.com, Experian.com, and TransUnion.com – all offer free dispute portals

For each collection entry, document the following:

- Original creditor name and account number

- Collection agency name (may differ from the original creditor)

- Original date of delinquency, this is when the 7-year reporting clock started

- Reported balance, check whether the amount has been inflated

- Account status: unpaid, paid, disputed, or in collections

- Scheduled removal date, 7 years from the original delinquency date

Step 2: Send a Debt Validation Letter Before Paying Anything

Before you pay a single dollar or accept any collection as valid, exercise your right to request debt validation. Under the Fair Debt Collection Practices Act (FDCPA), collection agencies must provide written proof that a debt is valid and legally collectible. This is one of the most underused, and most powerful, tools available to consumers.

To understand how collectors operate and how to use your rights against them, see our guide on Professional Credit Services: Know Your Rights – the same FDCPA protections apply to virtually every collection agency you’ll encounter.

Your validation letter should request:

- The name and address of the original creditor

- The exact amount owed, including all fees and interest added

- The original date of delinquency

- Proof that the collection agency has the legal right to collect this specific debt

- A copy of the original signed agreement (if applicable)

Once you send a validation request, the collection agency must stop all collection activity, including reporting, until they provide the required documentation. If they cannot validate the debt, they are legally required to cease reporting it and it must be removed from your credit file.

Step 3: Dispute Inaccurate Collections Under the FCRA

The Fair Credit Reporting Act (FCRA) gives you the right to dispute any inaccurate, incomplete, or unverifiable information on your credit report. This is one of the most powerful tools available, and it’s completely free to use.

Common errors that qualify for FCRA disputes:

- Wrong account balance or inflated amount

- Incorrect original delinquency date (re-aging a debt is illegal)

- Account doesn’t belong to you (identity mix-up or fraud)

- Same debt reported by both original creditor AND collector simultaneously

- Account past the 7-year reporting limit but still appearing

- Incorrect account status (shows unpaid when you’ve paid)

- Wrong creditor name or account number

How to file a dispute:

- File online at each bureau’s dispute portal, or by certified mail for a stronger paper trail

- State the specific reason: “The balance reported is $X but the correct amount is $Y”

- Include supporting documentation (bank statements, letters, receipts)

- File with ALL three bureaus, don’t assume they share dispute information

- Keep copies of everything and track your submission dates

Once you file a dispute, the credit bureau has 30 days (extendable to 45 if you submit additional information) to investigate. If the collection agency cannot verify the accuracy of the reported information within that window, the item must be corrected or removed entirely.

Step 4: Negotiate a Pay-for-Delete Agreement

If the debt is valid, current, and verified, a Pay-for-Delete agreement may be your best strategy. This is a negotiation where you agree to pay the collection balance, sometimes for less than the full amount owed, in exchange for the agency agreeing to completely delete the account from all three credit bureaus.

How to negotiate a successful Pay-for-Delete:

- Never call first, start with a written letter so everything is documented

- Offer 25–50% of the balance to start (collectors often purchased the debt for pennies on the dollar)

- Make your offer explicitly contingent on deletion, not just “paid” status

- Get the agreement in writing on the collector’s letterhead BEFORE sending any payment

- Pay by money order or cashier’s check, never give direct bank access

- Follow up in 30 days to confirm the deletion has been applied to all three bureaus

For a deeper comparison of your options, see our guide on Pay-for-Delete vs. Paid in Full – it explains exactly how each strategy affects your credit score and long-term financial standing.

Step 5: Request a Goodwill Deletion (For Paid Collections)

If you’ve already paid a collection but it’s still showing on your report, a Goodwill Letter is your best option. This is a written request asking the collection agency or original creditor to remove the paid collection as a gesture of goodwill.

When goodwill deletions work best:

- You have an otherwise strong payment history with only one or two isolated incidents

- The collection was paid in full (not settled for less)

- You can explain a specific hardship (job loss, medical emergency, divorce)

- You’re writing to the original creditor, not just the collection agency

There is no guarantee a goodwill deletion will be granted, it is entirely at the creditor’s discretion. However, many consumers are surprised to find that a well-written, sincere letter explaining their circumstances does result in removal. The cost is nothing but time, so it’s always worth attempting.

Step 6: Wait Out the 7-Year Reporting Period

If none of the above strategies succeed, the collection will eventually fall off your report on its own. Collection accounts must be removed after seven years from the original delinquency date, the date of the first missed payment that led to the collection, not the date the debt was sold.

Key rules about the 7-year clock:

- The clock starts from the original delinquency date, not when the collection agency bought the debt

- Paying a collection does NOT reset or extend the 7-year clock

- Re-aging a debt (misreporting the delinquency date to extend reporting time) is illegal under FCRA

- Medical collections under $500 were removed from reports under 2023 CFPB guidance

- Making a payment on a very old debt can restart the statute of limitations for lawsuits, know your state’s laws

Dealing With a Specific Collection Agency? We Have Dedicated Guides

Different collection agencies use different tactics, and some have specific vulnerabilities in the validation and dispute process that a knowledgeable approach can exploit. If you’re dealing with a named collector, these resources go deeper:

- Account Resolution Services (ARS): How to Remove ARS Collections From Your Credit Report

- National Credit Systems (NCS): Everything You Need to Know About NCS Collections

- Credit Collection Services (CCS): CCS Collections — What You Should Know and How to Fight Back

Don’t see your collector listed? Our full library of collector-specific removal guides covers dozens of agencies. Start with a free credit consultation and our analysts will identify exactly which strategies apply to your situation.

Collections and Mortgage Qualification: What You Need to Know

If you’re preparing to buy a home, a collection account is more than a credit score problem, it can be the difference between qualifying and not qualifying for a mortgage. Most conventional lenders use FICO 8, which still penalizes paid collections. FHA guidelines often require that certain collections be resolved before closing.

Our credit repair for home buyers program is designed specifically for this situation. Our analysts understand mortgage underwriting requirements from the inside, because our team includes licensed Mortgage Loan Originators who know exactly what lenders need to see on your report at closing.

What makes mortgage-focused credit repair different:

- We work toward specific mortgage eligibility thresholds, not just a “higher score” in general

- We coordinate with your lender and realtor to align with your closing date timeline

- We prioritize the specific accounts that are blocking your loan approval

- We address all three bureaus simultaneously, mortgage lenders pull tri-merge reports

How The Phenix Group Can Help Remove Collections Faster

The strategies in this guide are all legitimate and can be attempted on your own. But the process is time-consuming, legally nuanced, and easy to get wrong in ways that can actually weaken your position or, in the case of older debts, expose you to legal risk.

The Phenix Group uses an attorney-engaged credit repair process that goes far beyond generic dispute letters. Our specialists are trained in FCRA, FDCPA, and mortgage underwriting requirements, meaning we understand not just what can be disputed, but what needs to be resolved to get you to closing.

What sets The Phenix Group apart:

- Attorney-engaged process, all disputes are grounded in consumer law, not generic templates

- We engage original creditors, collection agencies, AND all three bureaus simultaneously

- Custom strategy for each client, not a one-size-fits-all approach

- Mortgage-focused expertise, our analysts understand lender requirements and closing deadlines

- No guarantees of specific outcomes, we promise transparency and expert execution

Want to see what’s possible? Browse real client results and success stories, or read more about our story and approach.

Serving Clients Nationwide, Including These Local Communities

Although The Phenix Group is a nationwide credit repair company, we provide hands-on, personalized service through local offices. If you’re looking for credit repair close to home, we have dedicated teams serving:

- Fort Worth, TX Credit Repair – serving Fort Worth, Arlington, Mansfield, and surrounding areas

- Dallas, TX Credit Repair – serving Dallas, Plano, Irving, and the greater DFW metro

- Austin, TX Credit Repair – serving Austin, Round Rock, Cedar Park, and Central Texas

Frequently Asked Questions (FAQ)

Can I remove a legitimate collection from my credit report?

Possibly. Even accurate collections can sometimes be removed through a Pay-for-Delete negotiation, a Goodwill Letter (if already paid), or if the collector cannot verify the debt during a validation request. However, if the collection is accurate, verified, and current, it may need to remain until the 7-year window expires.

Does paying a collection remove it from my credit report?

No. Paying a collection only changes the status from “unpaid” to “paid” – the account still remains on your report for the full seven years. This is why negotiating a Pay-for-Delete before paying is almost always the better strategy.

How long does a collection stay on my credit report?

Seven years from the original date of delinquency, the date you first missed a payment with the original creditor. This clock is not reset by payments, sales to new collectors, or any other activity after that original missed payment date.

Can I dispute a collection I actually owe?

Yes. You can dispute a collection if there are any inaccuracies in how it’s being reported, wrong balance, wrong date, wrong status, or reporting by both the original creditor and collector simultaneously. However, you cannot dispute a collection simply because you don’t want it there. The dispute process requires a factual basis.

What is the CFPB and how can they help?

The Consumer Financial Protection Bureau (CFPB) is a federal agency that protects consumers in financial transactions. If a collection agency violates your rights under the FCRA or FDCPA, for example, by failing to investigate a valid dispute or re-aging a debt, you can file a complaint at ConsumerFinance.gov. In cases of serious violations, you may be entitled to damages.

Should I hire a credit repair company to remove collections?

For simple cases, one or two collections with clear inaccuracies, you may be able to handle disputes on your own. For complex situations involving multiple accounts, mortgage preparation, or collections from multiple agencies, working with a professional credit repair company like The Phenix Group can save significant time and improve outcomes through attorney-engaged strategies that most consumers can’t replicate alone.

What’s the difference between a collection removal and a paid collection?

A collection removal means the account is completely deleted from your report, as if it never existed, this is the best outcome. A paid collection means the account stays on your report but shows a “paid” status. While “paid” looks better than “unpaid” to some lenders, it still shows up as a negative mark and can affect your score on older credit scoring models.